2025 China Marketing Market Insights: Five Consumer Trends Reshaping Marketing Strategy

- See Qian

- 2 days ago

- 5 min read

China’s marketing logic is shifting from selling products to proving value. Consumers are no longer choosing mainly on price or basic function. They are placing more weight on emotional comfort, better experiences, appearance confidence, health reassurance and smart convenience. That makes 2026 less about pushing features and more about showing why a product feels worth it in everyday life.

Why China consumer value is changing in 2025

The real shift is not that consumers have become less rational. It is that value now includes emotion, lifestyle fit, trust and self-expression alongside product performance. Age also plays a clear role in this shift, which means brands need sharper audience framing rather than one-size-fits-all messaging.

Data source: QuestMobile GROWTH User Profile Tag Database, December 2025; NEW MEDIA Database, December 2025

1) Emotional consumption is now the strongest consumer theme

Emotional consumption is the biggest of the five themes, but this is not just about impulse or mood-led spending. The report shows that brands are turning products into emotional carriers through three layers: creating emotion, connecting emotion and expressing emotion. In practice, that means stronger IP positioning, deeper storytelling, celebrity or creator amplification and collaboration-based marketing that turns products into social currency.

Data source: QuestMobile NEW MEDIA Database, December 2025

Toy and pop culture categories are one of the clearest examples. Brands are investing more heavily in IP-led demand, while building emotional value through world-building, character development and stronger cultural positioning. At the same time, celebrity partnerships are moving beyond one-off endorsement into deeper brand association.

Key data points:

Toy-sector hard-ad spend in 2024: RMB 448.52 million

Toy-sector hard-ad spend in 2025: RMB 601.62 million

Year-on-year growth: +34.1%

Food and beverage brands are also using mature IP collaborations to speed up conversion. The report notes that campaigns such as Luckin x Honkai and KFC x Genshin reached more young, female and lower-tier market users, helping brands extend beyond their existing base.

2) Experience-led marketing is becoming a growth driver

Experience consumption is now the second-biggest theme, and travel sits at the centre of it. This is shift from buying a product to buying into an experience, especially visible in travel, live entertainment and outdoor activity, where consumers are paying for the process, the atmosphere and the memory as much as the item itself.

Data source: QuestMobile NEW MEDIA Database, December 2025

Travel is the clearest commercial example. The report says the sector now carries “experience” through the full marketing chain, from the timing of ads around decision windows to content that captures immediate interest and makes trips feel more personalised. The important shift is that travel brands are moving beyond price-war logic and making distinctive experiences the new competitive edge.

The same trend appears in sportswear, where brands are increasingly selling outdoor lifestyle aspiration rather than equipment alone.

Outdoor experience content data:

Outdoor running interaction share: 9.9%

Hiking interaction share: 5.4%

Basketball interaction share: 4.3%

Marathon interaction share: 4.2%

Badminton interaction share: 4.2%

For brands, the opportunity is to show the scene as clearly as the product, make experience central to the value message and, especially in travel, sell distinctive moments rather than discounts alone.

3) Appearance value is driving premium consumer behaviour

Appearance consumption is about more than looking good. The report defines it as paying a premium for beauty, with brands turning external value into purchase motivation through social image, self-reward and better product aesthetics. The report groups this into three routes: to please others (悦TA), to please yourself (悦己)and to please through the product itself (悦它). The key message is simple: design, image and visual appeal are now strong drivers of purchase.

Beauty provides the clearest proof, but the logic extends well into luxury. Under “to please yourself” (悦己), the report shows that luxury brands are using appearance value to reinforce premium positioning through gifting moments, self-reward occasions, celebrity-led storytelling and cultural experiences. In other words, premium value is no longer built on aesthetics alone. It is built on how brands attach beauty to status, ritual, aspiration and emotional payoff.

Luxury brands are also building appearance value offline. They are using cultural embedding, local creativity and experiential spaces to add brand meaning and reinforce scarcity. This shifts premium marketing beyond beautiful products alone, making appearance feel stronger when it is supported by story, setting and a sense of exclusivity.

Key appearance value data

Efficacy skincare interaction share: 26.1%

Seasonal make-up interaction share: 11.4%

Light make-up interaction share: 5.8%

The opportunity for brands is to treat design as part of the product value, use visuals and packaging as conversion tools, and frame appearance as confidence and identity rather than vanity alone.

4) Health reassurance is becoming everyday consumer value

Health consumption is now firmly mainstream. Rather than being a reactive health trend, it is becoming part of daily lifestyle management. Consumers are moving from “seek treatment when ill” towards ongoing health routines, which creates more room for brands that can build trust, fit into habits and make wellbeing feel practical and repeatable.

Health and wellness posting volume on content platforms stayed broadly stable throughout 2025. That suggests awareness is already there. The bigger change is behavioural: consumers are becoming more interested in self-management, measurable routines and professionalised daily health behaviour.

Key health consumer trend data:

Health consumption search penetration: 12.9%

By age group, health-related content search rates were 14.1% for age 19–30 users, 13.7% for age 31–50 users and 12.5% for age 50+ users.

The strongest health brands will make wellbeing feel trusted, routine-led and naturally part of everyday life, rather than something triggered by fear.

5) Smart convenience is still part of the value shift

Smart convenience may be the smallest of the five themes, with search penetration at 3.9%, but it still plays an important role in how consumers define value. Smart consumption around efficiency, safety and convenience, which means the appeal is less about owning advanced technology for its own sake and more about making everyday life easier.

The report also notes that smart consumption users are growing, with post-80s and post-90s consumers now the main spending force. That gives brands a useful direction: smart value works best when it feels relatable and visible in daily routines, whether through AI services, smart mobility or connected home experiences.

The commercial takeaway is straightforward. Brands do not need to over-explain the technology. They need to show how it improves everyday living in a way consumers can immediately understand and justify.

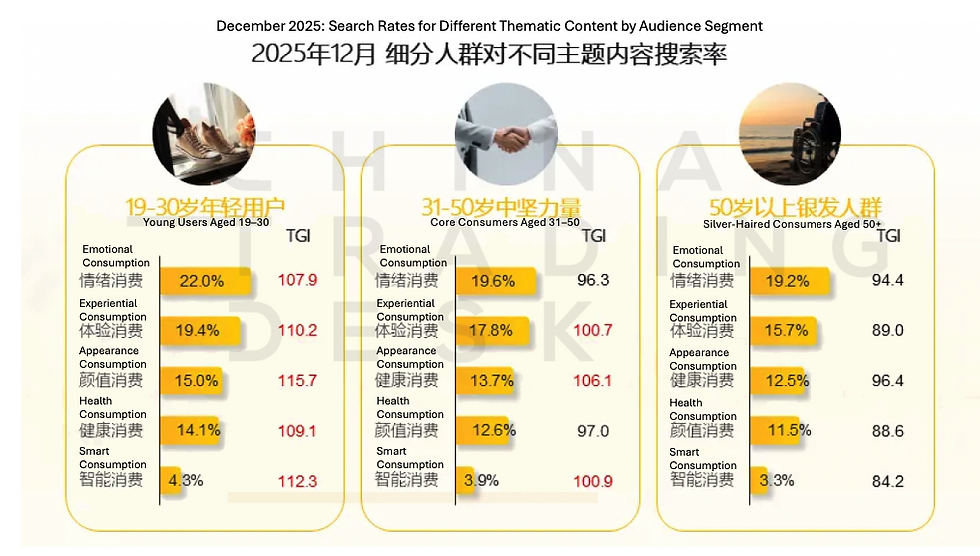

Age differences are reshaping marketing strategy

Age is one of the clearest clues to how value is being redefined in China. Emotional consumption ranks first across all age groups, but the shape of interest shifts noticeably by life stage. Younger consumers lean more strongly into experience, appearance and smart content, while the 31 to 50 group shows a relatively stronger pull towards health-led value.

Data source: QuestMobile GROWTH User Profile Tag Database, December 2025; NEW MEDIA Database, December 2025

For brands, that means broad messaging is becoming less effective. Younger audiences respond better to identity and shareable experiences, while older audiences are more likely to value reassurance, practicality and wellbeing.

What this means for China marketing strategy in 2026

The main lesson is simple: China’s consumers still care about value, but value now includes far more than price and performance. Emotional connection, quality of experience, appearance confidence, health reassurance and convenience are all shaping what feels worth buying.

Quick summary

Emotional consumption is the leading theme

Experience is becoming a key selling lever

Appearance and health are shaping premium decisions

Smart convenience is a smaller but important growth area

Age-based targeting is now essential

Get in touch with us to sharpen your positioning, align your campaigns with what consumers value most and stay ahead in China’s changing market.

Comments