China Luxury Market Outlook: Key Trends Shaping the RMB 1 Trillion Opportunity

- See Qian

- Mar 19

- 7 min read

China’s luxury market is entering a new phase of growth—one defined not just by scale, but by smarter conversion, stronger domestic consumption, digital discovery, and premium travel experiences.

According to recent market research, China’s luxury market is projected to surpass RMB 1 trillion, with annual growth expected to remain at 8% to 10% in the coming years. Growth is being supported by younger consumers, digital commerce, policy support, improved domestic retail infrastructure, and the continued reflow of luxury spending back into China.

Data Source: Qianzhan Industry Research Institute

For luxury brands, hotels, airlines, airports, and travel retail operators, the key question is no longer simply where Chinese consumers buy luxury goods. It is how they move across social platforms, ecommerce, physical stores, domestic travel, and premium service environments before deciding to purchase.

This newsletter highlights the most important signals from the China Luxury Goods Industry Market Research Report, and updated with our latest China Outbound Travel Q1 2026 insights, and translates them into practical implications for businesses operating in luxury retail, travel retail, hospitality, aviation, and premium customer experience.

Luxury vs High-End: Why the Distinction Matters

Luxury goods and high-end consumer goods are often grouped together, but they operate on very different value drivers.

High-end consumer goods focus on:

product quality

durability

functionality

everyday performance

Luxury goods, by contrast, are defined by:

brand heritage

exclusivity

cultural symbolism

emotional and identity value

In simple terms, high-end products are purchased to improve life through performance. Luxury goods are purchased not only for quality, but also for identity, aspiration, and emotional value.

This distinction matters because luxury conversion depends far more on storytelling, controlled brand environments, premium service, and trust, while high-end consumer goods can compete more directly on product benefits, usability, and long-term value.

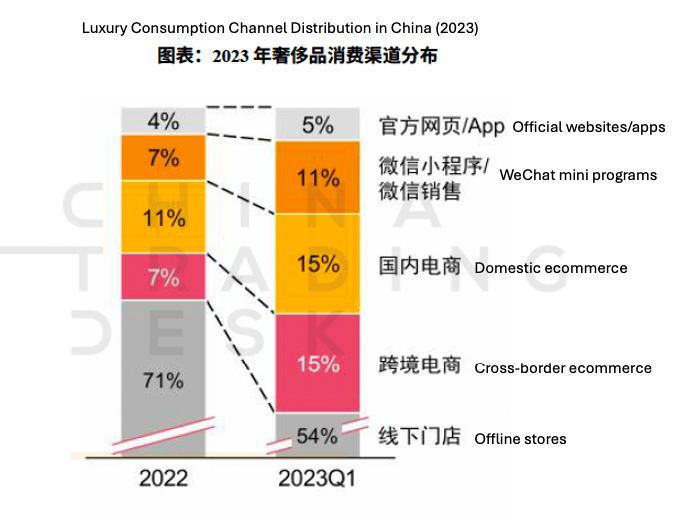

China’s Luxury Market Is Becoming Domestic-First

One of the most important structural shifts in China’s luxury sector is the reflow of consumption back to the domestic market.

For years, Chinese luxury consumption relied heavily on overseas travel shopping and daigou channels. But policy changes, better domestic duty-free conditions, stronger retail infrastructure, and improved onshore brand presence have gradually pulled more spend back into China.

Data Source: Bain & Company, 2024 China Luxury Market Report

Even as outbound travel continues to recover, domestic luxury consumption is no longer just a substitute for overseas shopping. For many consumers, it is becoming a preferred route because of:

easier access

stronger service confidence

more mature domestic retail environments

better integration with digital channels

Cross-border ecommerce is also continuing to reduce friction by widening access while maintaining convenience.

Q1 2026 update: digital discovery and travel retail are reshaping China’s luxury market

Our latest Q1 2026 survey shows that China’s luxury market opportunity remains strong, but is becoming more selective, deliberate, and conversion-led.

Short-term outbound travel intent eased slightly to 21.6%, down from 22.9% in Q4 2025. However, airport travel retail interest remained resilient at 64.3%, showing that premium shopping demand is still holding within the travel journey, even as consumers become more intentional about when and where they spend.

The strongest opportunity continues to sit with affluent and younger travellers, reinforcing the importance of targeting consumers who are both digitally engaged and comfortable moving between premium retail and travel environments.

Just as importantly, the luxury journey remains hybrid. Most travellers still shop mainly in downtown locations, but many also purchase at the airport, making travel retail an important extension of luxury conversion rather than a standalone channel.

For operators, this has clear implications. Beauty, fashion, and fragrance remain the most commercially relevant premium categories, while assortment visibility, trusted pricing, and seamless digital-to-physical experiences are becoming more important than promotions alone.

Category mix shows where brands, hotels, and travel retail can monetise fastest

The report highlights the current category structure of China’s luxury market:

Fashion: ~40% of the market

Jewellery: ~25%

Watches: ~15%

Beauty & lifestyle luxury: ~20%

Each category behaves differently across retail, hospitality, and travel environments.

Fashion: The Traffic Driver

Fashion remains the largest segment and plays a key role in building brand visibility, aspiration, and retail traffic.

Jewellery & Watches: Trust-Based Purchases

Jewellery and watches carry strong symbolic, investment, and inheritance value, especially among high-net-worth consumers.

These categories typically require:

slower purchase consideration

stronger consultation

higher service reassurance

more private retail environments

Beauty & Lifestyle: Ideal for Travel Retail

Beauty and lifestyle luxury products are particularly well suited for travel retail and hospitality because they are:

portable

replenishable

easier to integrate into service experiences

Data source: Bain & Company, 2024 China Luxury Market Report

Digital Discovery Is Rising — But Physical Experience Still Converts

China’s luxury market is becoming increasingly digital, but it is not becoming purely digital.

Data source: PwC

Industry forecasts suggest that by 2025:

Online luxury sales: 35–40%

Offline luxury retail: 60–65%

Consumers continue to value in-person experiences, including:

product fitting

tactile interaction

personalised consultation

At the same time, online-to-offline (O2O) retail models are expanding rapidly through services such as:

online reservations

in-store collection

virtual try-on

customised consultations

The takeaway is clear:

Digital channels start the luxury journey but physical service completes it. This is especially relevant in China, where digital discovery increasingly drives footfall into stores, hotel retail partnerships, and airport luxury environments.

Gen Z and Millennials Are Redefining Luxury Consumption

Consumers aged 25 to 40 remain the dominant force in China’s luxury market, with Gen Z and Millennials driving demand through stronger interest in innovation, individuality, and self-expression.

These consumers are not only buying luxury goods for ownership. They are also buying for:

personal identity

social visibility

cultural relevance

emotional resonance

Compared with older luxury buyers, younger consumers are more attentive to a brand’s creative design, cultural narrative, innovation, and values. They are also more likely to engage with limited editions, collaborations, and socially shareable experiences.

This means luxury operators must think beyond product display. They need to create environments that support curation, expression, and storytelling.

Data source: iiMedia Research

Social Platforms Are Now Part of the Luxury Sales Infrastructure

As digital natives, Gen Z and Millennials rely heavily on online channels and social media platforms throughout the luxury purchase journey.

Key platforms shaping luxury discovery and purchase decisions include:

Xiaohongshu (RED)

Douyin

Weibo

WeChat

Through influencer content, livestream commerce, and user-generated reviews, consumers can:

evaluate product experiences

build brand trust

make faster purchase decisions

In this environment, digital content is no longer just a marketing layer. It has become part of the sales infrastructure.

For luxury brands and premium operators, digital ecosystems now serve as the bridge between brand storytelling, customer engagement, personalisation, and commercial conversion.

Policy and Trust Will Continue to Shape the Market

China’s luxury sector is also influenced by ongoing policy and regulatory developments.

The report highlights several factors shaping the market environment:

import tariff adjustments

cross-border e-commerce support

stronger intellectual property protection

consumption-stimulating policies

At the same time, macroeconomic uncertainty and global trade shifts remain part of the landscape. That makes trust even more commercially important.

In luxury, trust is not only reputational. It is operational. It influences conversion, repeat purchase, and channel choice. Consumers increasingly expect:

authenticity assurance

transparent pricing

reliable after-sales service

consistent premium service across channels

The operators that perform best in China’s next luxury phase are likely to be those that combine policy awareness, service reliability, and brand confidence into one seamless experience.

Key Future Trends in China’s Luxury Market

China’s luxury growth is unlikely to come from scale alone. It will increasingly depend on a more refined model built around personalisation, sustainability, digital integration, and cross-sector collaboration.

Personalisation and Customisation

Consumers are looking for products and services that reflect their identity, preferences, and lifestyle. Digital tools such as VR, AR, and smarter production systems are making tailored luxury experiences more scalable.

Sustainability and Responsible Luxury

Consumers are paying closer attention to environmental standards, ethical production, and supply chain transparency. More are willing to pay a premium for products and experiences that align with these values.

Cross-Sector Collaboration

Luxury is becoming more connected to technology, art, culture, hospitality, and immersive digital formats. This expands where and how luxury can be discovered, experienced, and sold.

Stronger CRM and lifecycle engagement

The next phase of growth will reward brands that sharpen positioning, deepen storytelling, strengthen service across the full purchase cycle, and use membership and customer data more effectively to support loyalty.

What This Means for Luxury Retail, Travel, and Hospitality

Luxury retail: focus on omnichannel and customer insight

Success will depend less on broad awareness and more on connected online-to-offline experiences, category-specific conversion strategies, and stronger CRM.

Airports and airlines: reposition travel retail

Travel retail should be treated as a premium service ecosystem that enhances the journey, rather than simply a transactional sales channel. The Q1 2026 data shows that airport luxury demand remains resilient, even as consumers become more selective.

Hotels: expand into curated commerce

Hotels have opportunities to capture guest intent before arrival, facilitate luxury discovery during the stay, and enable post-stay repurchase through partnerships, concierge-led retail, premium amenities, and curated commerce experiences.

Premium operators: win through trust and convenience

Across sectors, assortment visibility, transparent pricing, digital discovery, and seamless physical fulfilment are becoming stronger drivers of conversion than promotions alone.

Younger consumers are shaping luxury expectations

Gen Z and Millennials expect relevance, convenience, storytelling, and premium service to work together across retail, social platforms, and travel experiences.

Conclusion

China’s luxury market is entering its next phase with greater scale, stronger domestic foundations, and deeper structural integration across retail, digital commerce, social influence, and premium travel environments.

The projected move beyond RMB 1 trillion is significant, but the more important story is how luxury consumption is being reorganised. Discovery increasingly starts online. Trust is built across channels. Conversion happens across a mix of downtown retail, ecommerce, airport environments, and premium service settings.

The latest Q1 2026 update reinforces that the market remains attractive, but it is becoming more selective. Consumers are still willing to spend, especially in travel and premium categories, but they expect stronger visibility, better curation, trusted pricing, and more seamless journeys between digital discovery and physical purchase.

For brands and operators in luxury retail, hospitality, aviation, and travel retail, the opportunity is no longer only to sell luxury goods. It is to create the conditions in which luxury conversion feels easier, safer, more personal, and more experience-led.

In China’s next luxury cycle, the journey is no longer separate from the purchase. It is part of the purchase.

If your brand is looking to translate China’s luxury growth into a sharper retail, travel retail, hotel, or premium service strategy, get in touch with us.

Comments