From Traffic to Trust: The China Marketing Trends Defining 2026

- See Qian

- 2 days ago

- 5 min read

China’s marketing market is still growing, but it is growing up

QuestMobile’s 2025 China marketing market report makes one point very clearly: China’s marketing industry is not slowing down, but it is becoming more mature, more disciplined and more performance-led. Growth is still there, yet the conditions for winning have changed. Regulation is firmer, consumers are more layered, and advertisers are under more pressure to prove commercial value.

The report ties this new phase to two structural forces. First, China’s consumer economy has remained on a stable recovery track. Second, the shape of the internet population is changing, with older users becoming a more important growth group. Together, those two shifts are changing what users buy, how they decide, and where brands need to show up.

Key market figures:

Internet advertising market size in 2023: RMB 714.61 billion

Internet advertising market size in 2025: RMB 793.08 billion

Forecast for 2026: RMB 836.26 billion

Forecast for 2027: RMB 884.76 billion

What makes this especially important is that growth is not being driven by media scale alone. The report links advertising resilience to two deeper forces: steady consumer recovery and structural changes in who China’s internet users now are. In practical terms, marketers are dealing with a market that is bigger, but also more layered, more rational and less forgiving of waste.

Consumer spending is now running on two tracks

One of the most useful sections in the report is its view of consumption. Chinese consumer demand is increasingly being shaped by both functional necessity and emotional interest. In simple terms, people are spending both on what they need and on what gives them pleasure, identity or emotional payoff.

This matters because it changes the kind of messaging that works. A purely rational price-and-performance approach is no longer enough in every category. At the same time, emotion without utility is not enough either. The market is asking brands to work harder across both value and feeling.

The report highlights:

China’s total retail sales of consumer goods in 2025 reached RMB 50.1 trillion

Year-on-year growth was 3.7%

User preference showed simultaneous uplift in:

just-in-case stock-up demand

interest and emotional-value consumption

Meanwhile, the content environment is shifting with it. Experiential and service-led consumption content is rising in popularity, and that AI and automotive are acting as dual engines of content traffic. That is an important signal for marketers. The consumer is not just buying products. They are increasingly responding to experiences, scenes and relevance.

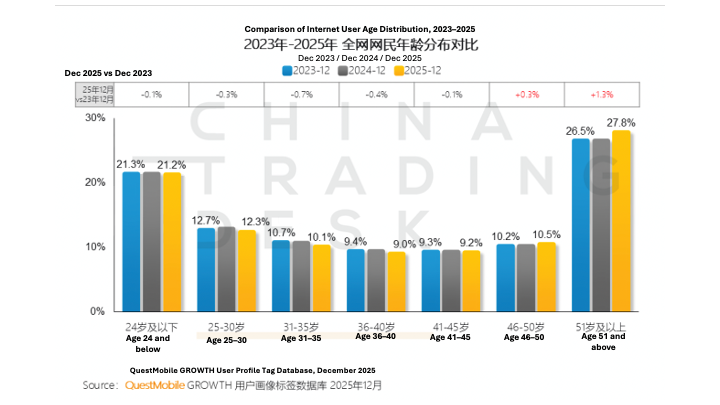

China’s internet audience is changing shape

The report also shows that China’s internet population has entered what it calls a more stable age-structure phase. But stable does not mean static. The strongest structural increase is coming from older users, especially the silver generation.

This is commercially significant because older audiences are not simply adding volume. They are also reshaping online behaviour, digital trust patterns and purchase expectations. Younger users remain the foundation of the market, but the next layer of growth is broader and older.

The demographic signal to watch:

Users aged 46+ accounted for 38.3% of all internet users in 2025

That was up 1.6 percentage points versus 2023

For brands, the implication is clear. China’s digital market can no longer be read through a youth-only lens. Marketers need messaging, formats and journeys that work across generations, especially where service, reassurance and practical value matter.

Advertisers are rebuilding budgets around performance and brand value

Source: QuestMobile AD INSIGHT Advertising Data Database, December 2025

China’s advertising market has entered a phase of rational budget reconstruction, with brands placing greater weight on measurable outcomes, real conversion and stronger commercial certainty. That does not mean brand investment is disappearing. It means every line of spend is being judged more rigorously.

Traditional industries are leaning more heavily towards performance-led media, using sales and effectiveness as the clearest benchmarks for channel selection.

Internet advertisers, by contrast, are increasing the share of brand advertising as they try to reduce reliance on pure traffic buying and rising customer acquisition costs. From 2023 to 2025, brand ad share in traditional industries fell from 21.3% to 17.1%, while the share for internet industries rose from 4.8% to 13.0%, including a 6.1 percentage-point increase versus 2024.

China’s digital advertising market is no longer following one budget logic. Traditional sectors are buying harder for results, while internet players are using brand-building as a growth lever in a more competitive market.

IP and emotion are becoming stronger growth levers in China marketing

Source: QuestMobile Marketing Insights Institute, March 2026

Report also shows that IP marketing is moving closer to the centre of brand strategy. IP marketing now account for 63.3% of brand marketing event ads, while festival marketing 31.3%, making them the two strongest engines in the IP mix. That matters because brands are no longer using IP simply to gain visibility. They are using it to strengthen relevance, speed up recognition and improve brand recall in a more crowded media environment.

Emotion is becoming just as important in China digital marketing trends. The report shows that emotionally resonant themes can generate rapid increases in engagement when they connect with identity, empathy and self-recognition. For brands, the commercial lesson is clear:

IP helps capture attention

Emotion helps deepen engagement

Together, they improve both visibility and memorability

In practical terms, brands in China are no longer competing only on reach. They are competing on whether the message feels culturally relevant, emotionally timely and easy for audiences to connect with and share.

AI marketing in China is becoming more recommendation-led

Source: QuestMobile TRUTH China Mobile Internet Database, February 2026; QuestMobile Marketing Insights Institute, March 2026

AI marketing in China is moving away from broad exposure and towards smarter recommendation, stronger demand matching and faster action. The report says AI-native apps are reshaping traffic and monetisation, with user entry shifting from manually opening apps to AI recommendation and wake-up. AI-native app usage frequency rising to around 150 by January 2026, reinforcing that AI behaviour is becoming more embedded in everyday digital use.

Key takeaway:

Less about traffic

More about recommendation

More about timing and conversion

Conclusion: China’s marketing market is moving beyond simple exposure

China’s marketing market is entering a more mature phase. Growth remains intact, but the logic behind that growth is changing. The market is moving away from pure traffic and broad exposure towards a model shaped more by experience, trust, recommendation, timing and conversion.

What makes this shift important is that it is happening across the full marketing chain at once. Consumer demand is becoming more layered, media entry points are being reshaped by AI, emotionally resonant content is gaining more weight, and marketing is becoming more embedded in everyday scenarios. This is not a short-term adjustment in media planning. It is a broader reset in how marketing works in China.

The report’s forward-looking direction can be read through four connected shifts:

Experience-first marketing

Earlier demand recognition and better timing

AI-led entry points and upgraded user access

Scenario-based and IP-led integrated exposure

In short, China’s marketing market is no longer being defined by who can generate the most visibility. It is increasingly being defined by who can create the most relevant, credible and efficient path from attention to action.

If you want to turn China marketing trends into a stronger 2026 media and growth plan, get in touch with us.

Comments