Inside China’s 2025–26 Outbound Travel Shift: How Consumer Behaviour and Digital Trends Are Reshaping Global Tourism

- Xin Hui

- Dec 10, 2025

- 5 min read

ITB China Tourism Trend Report 2025/26 presented that China’s outbound travel market is entering a new phase of accelerated recovery and structural transformation.

A New Global Growth Cycle — Led by Asia Pacific and Powered by China

The global tourism sector has entered a new and optimistic growth cycle. In 2024:

International overnight trips reached ~1.5 billion

Inbound visitor nights exceeded 2019 levels by 5%

Tourism spending rose to US$1.6 trillion, up 11% year-on-year

While recovery remains uneven across regions, Asia Pacific stands out. According to Tourism Economics, it is expected to deliver the strongest inbound and outbound growth globally through 2027, driven largely by China’s resurgent cross-border travel.

For global tourism businesses, China’s outbound recovery is no longer a forecast, it is an active market force reshaping demand patterns worldwide.

China’s Outbound Travel Reaccelerates: Bigger, Younger, and More Diverse

2024 marked a decisive rebound

Mainland Chinese residents made over 145 million outbound trips in 2024, with overseas spending climbing to 5.75 trillion RMB, a 17% year-on-year rise.

Travel confidence is strong with 74% of ITB China buyers expect 2025 outbound business to exceed 2024, while only 5% foresee a decline.

Trip.com booking data reinforces this momentum. In Q4 2024, outbound hotel and flight bookings surpassed 2019 levels by over 20%, signalling not just recovery, but growth beyond pre-pandemic benchmarks.

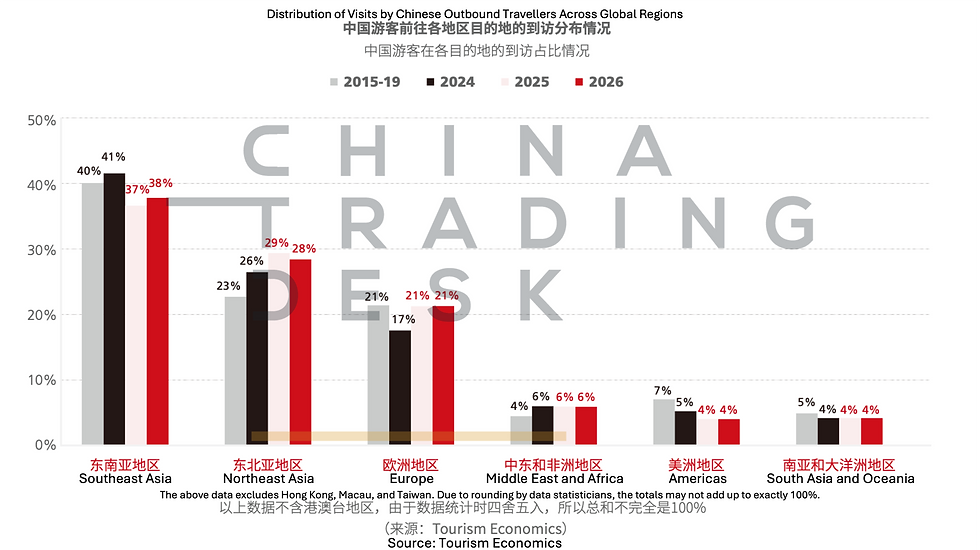

Where Chinese travellers are going in 2025

Analysis across destination tourism boards and Trip.com data reveals that:

37% of mainland outbound overnight visitors choose Southeast Asia

29% choose Northeast Asia

21% head to Europe

Top outbound destinations include: Singapore, Thailand, South Korea, Malaysia, Australia, Indonesia and more.

A younger demographic is driving demand

China’s outbound travellers are overwhelmingly under 45:

36%: 80s generation

31%: 90s generation

10%: 00s generation

These digital-native cohorts embrace technology, value flexibility, and are open to niche experiences, reshaping both product design and destination marketing.

What Chinese Travellers Want Now: From Immersion to Precision

1. FIT is now the mainstream model

One of the strongest behavioural shifts is the move away from traditional group tours.

Travel agency leaders interviewed by ITB China confirm:

Large group tours are declining

Visa centres are overwhelmed with individual applications

Long-haul FIT is growing rapidly, especially for Europe, Japan, and Australia

Travellers want independence, control, and customisation, not fixed itineraries.

2. Authenticity and immersion drive destination decisions

Trip.com’s data shows that travellers booked 1,000+ new attractions in 2024 versus 2019, reflecting:

Curiosity for local culture

Interest in “newness” and under-the-radar experiences

Desire for real, unfiltered encounters

From food trails and craft workshops to nature-based itineraries, demand for immersive products has never been stronger.

3. Destination horizons are expanding

Chinese travellers are increasingly exploring beyond classics.

In 2024, travellers booked tickets for 120 more destinations than in 2019.Growth hotspots include:

Middle East (UAE, Saudi Arabia)

Central Asia (Kazakhstan, Uzbekistan)

Mediterranean and Balkan regions

4. High willingness to spend, especially on experiences

China remains one of the world’s highest-spending travel markets.Chinese travellers’ per-night overseas spend exceeds all major markets, including the US, Germany, and Japan.

Top Travel Themes Chinese Travellers Are Willing to Spend On:

Family & kids travel (61%) – Spending is strong for multi-generational trips, child-friendly attractions, private transfers, and convenience-focused accommodations.

In-depth urban exploration (60%) – Travellers pay for local guides, neighbourhood tours, cultural walks, and premium dining in major global cities.

Island leisure (38%) – Strong willingness to spend on beachfront resorts, water activities, photography experiences, and wellness add-ons.

Culinary & food culture (33%) – Food-themed itineraries, cooking workshops, and destination dining continue to attract premium budgets.

Cultural & educational travel (33%) – Young adults and families invest in museums, heritage experiences, and specialised tours.

5. The rise of the silver traveller

China’s ageing population — 310 million aged 60+ — is transforming the outbound landscape.The China Tourism Academy forecasts that by 2025, more than 100 million active seniors will influence the sector, with the silver travel market surpassing 1 trillion RMB.

Evidence shows that senior outbound orders grew 20% under Ctrip’s dedicated “Senior Club” offering.

For destinations and operators, this presents a major premium opportunity. Travellers who value comfort, safety, and meaningful experiences are now a core growth engine.

MICE & Corporate Travel: China’s Highest-Value Recovery Segment

China’s MICE and corporate travel market is expanding faster than many leisure segments.

Budgets are large and rising

ITB China’s MICE buyer survey shows:

35% of buyers manage more than 50 million RMB annual procurement budgets

20% manage 10–50 million RMB

18% expect 2025 company revenue above 100 million RMB

Pharmaceuticals, finance, government, manufacturing, and high-tech industries dominate demand.

Bleisure becomes a core growth driver

83% of buyers identify business + leisure travel as one of the most promising growth areas.BCD Travel reports 42% of business travellers extended stays in 2024, adding an average of 2.3 leisure days. This is reshaping:

Event design

Venue selection

Destination marketing

Supplier packages

ESG becomes a procurement requirement

Chinese corporates, particularly in international sectors increasingly demand:

Carbon-reporting tools

Greener venues and accommodation

Lower-impact event design

Social-impact integration

ESG is no longer a trend; it is a compliance expectation for global-facing Chinese corporations.

Regional Dynamics: Opportunities & Challenges

The report outlines distinct momentum and risks across regions:

Southeast Asia

Visa-free policies and short flight times fuel demand, though online fraud controversies may temporarily affect perceptions.

Northeast Asia

Japan and South Korea strengthen share with improved flight recovery and currency advantages.

Europe

Search volume surged—Italy doubled, and lesser-known destinations rose five-fold.Challenges include visa bottlenecks and longer flight times linked to geopolitical constraints.

Middle East and Africa

Luxury positioning, new infrastructure and economic ties support growth, though geopolitical risks remain.

Central Asia

A rising market driven by new infrastructure and cultural exploration.

Americas

Recovery is slower due to limited capacity and visa hurdles, yet family, education and business demand stay resilient.

Technology, AI, and the Future of China-Ready Travel

Travel brands and destinations are rapidly adopting digital tools.ITB China buyers report the highest adoption in:

AI-powered product recommendation (46%)

AI-assisted product development (40%)

AI-driven customer service (26%)

Data analytics (23%)

Digital marketing, CRM systems, mobile payments, and social-media-first storytelling remain essential for reaching China’s younger travellers.

What This Means for Destinations and Travel Brands

Personalisation is not optional, it is the default expectation

Travellers want itineraries shaped around their identity, not generic mass-market templates.

Experience value matters more than price

Consumers will pay for experiences that feel meaningful, immersive, and unique.

Silver travel requires specialist service innovation

Accessibility, care support, slower pacing, and health-led itineraries will define this demographic.

MICE is a priority growth engine

Bleisure, cross-border corporate expansion, and ESG-driven procurement are reshaping business travel needs.

Tech adoption is a discriminator

Brands that integrate AI, digital convenience, and mobile-first content will win younger audiences.

Conclusion

China’s outbound travel revival brings both scale and complexity. Success will depend on understanding demographic nuances, digital influence, regional dynamics, and evolving expectations for personalisation and safety.

Reach out to our team to learn how your brand can engage China's outbound market or to customise strategic solutions built around your market goals.

Comments