China Outbound Travel Outlook 2026: From Recovery to Market-Share Fight

- China Trading Desk

- 6 days ago

- 6 min read

CTD’s Q1-anchored outlook shows a China outbound market that is expanding again — but the commercial opportunity is concentrated in the destinations that can win higher-value trips, not just more arrivals.

The 2026 outlook is Q1-anchored, risk-aware, and built for commercial planning.

China outbound travel is no longer a question of whether demand returns. It is now a question of who captures the spend.

In 2026, the market is moving from recovery to allocation: which destinations win the next wave of Chinese travelers, which corridors capture the most value, and which brands influence decisions before the trip is booked.

This outlook is written for destination marketers, travel retailers, hotels, airlines, airports, attractions, and brands planning around Chinese outbound demand in 2026.

Our latest China Outbound Travel Market Outlook 2026 uses Q1 actuals, official China-side controls, destination inputs, aviation signals, payment-spend proxies, and risk scenarios to create a practical planning view for the year ahead.

The base case points to 178 million outbound trips and US$276.1 billion in in-destination traveler spend for FY2026. The high case reaches 187.3 million trips and US$295.9 billion. This refers to estimated spend in destinations and excludes international airfare.

Those numbers matter, but the larger commercial takeaway is that growth will not be evenly distributed. Some destinations will win on volume. Others will win on spend intensity, shopping-linked value, longer stays, or better access. The winners will be the markets and brands that shape traveler intent early, not only those waiting for demand to arrive.

What Q1 tells us

The outlook starts with what has already happened.

China’s National Immigration Administration reported 185 million cross-border entries and exits in Q1 2026, including 91.662 million mainland resident crossings. For planning purposes, this is treated as roughly 45.8 million mainland outbound trips in Q1, using a standard half-crossing method.

For spend, the outlook uses SAFE’s Balance of Payments travel-debit data as the macro control. Q1 2026 travel debit is anchored at US$64.6 billion across January to March.

The key point is that trips and spend do not follow the same seasonal pattern. Chinese New Year, May Day, summer holidays, Golden Week, route capacity, and destination mix all affect the rest of the year differently. A simple four-times-Q1 run-rate would overstate some areas and understate others.

That is why the forecast separates:

• observed Q1 trips from projected full-year trips;

• observed Q1 travel spend from projected full-year spend;

• core demand potential from risk-adjusted planning numbers.

Outbound recovery is broad, but the commercial opportunity is concentrated in corridors with access, experience, and spend potential.

The recovery is uneven

A strong total market does not mean every destination grows at the same pace.

Short-haul markets benefit from convenience, lower friction, repeat visits, and flexible trip planning. Hong Kong, Macao, Japan, South Korea, Thailand, Singapore, Vietnam, and other nearby markets remain central to outbound recovery because they are easier to access and easier to repeat.

Long-haul markets play a different role. Europe, the United States, Australia, the United Kingdom, and other premium corridors may not always lead on trip count, but they can matter disproportionately for spend per journey, longer stays, retail, hospitality, attractions, and services.

More travelers do not always mean more value. Spend intensity, stay pattern, and shopping intent can change the commercial ranking.

For marketers, this means the opportunity should be judged across three dimensions:

Demand scale — how many Chinese travelers a market can realistically attract.

Spend intensity — how much value each trip can generate.

Influence potential — how much of the trip decision and spend can be shaped through media, content, partnerships, retail, and pre-trip planning.

The strongest opportunities sit where these three factors overlap.

What changed from the earlier outlook

Our earlier 2026 outlook framed the market around a broad recovery scenario. The updated view is more useful for planning because it adds four refinements.

First, it uses Q1 2026 actuals instead of relying only on annual assumptions.

Second, it separates core potential from risk-adjusted planning. Core potential shows the demand opportunity before current disruptions. The risk-adjusted view accounts for oil and airfare pressure, Middle East routing disruption, capacity constraints, and partial destination substitution.

Third, it handles destination data more carefully. Some markets publish timely China-specific arrivals. Many do not. The live outlook therefore distinguishes named destination markets from regional opportunity pools, instead of pretending every row has the same data quality.

Fourth, it makes confidence visible. Total trips and total spend have stronger data coverage because they are anchored to official China-side sources. Country-level spend is more modeled because monthly spend by Chinese travelers is rarely published consistently by destination.

Country-level estimates should therefore be read as planning signals, not official destination receipts.

The 2026 planning range

The base planning view is constructive, but not risk-free.

Low case: slower momentum, more pressure from airfare, weaker discretionary demand, and higher disruption.

Base case: continued recovery, with current travel risks included.

High case: stronger Q2-Q4 momentum, better capacity, lower disruption, and higher spend capture.

This range is more useful than a single forecast. Destination teams, airlines, retailers, hotels, and brands need to know how their plans change if the year lands closer to a cautious recovery, a steady expansion, or a high-spend upside case.

The risks that matter most

The key risks are about conversion: whether traveler intent can turn into actual trips and spend.

Air capacity and route restoration. Demand can be capped by limited seats, weak direct connectivity, or inconvenient routing. This matters most for long-haul markets and corridors affected by Middle East connections.

Oil and airfare pressure. Higher fares can reduce marginal trips, especially for price-sensitive leisure travelers and families. In the outlook, this mainly affects trip volume and destination mix, rather than automatically increasing destination spend.

Middle East routing disruption. The risk is not only GCC destination demand. Middle Eastern hubs also support connections between China and Europe, Africa, and other long-haul markets. Some disrupted demand is lost, while some is redirected to Southeast Asia, North Asia, direct Europe routes, or other better-connected corridors.

FX affordability and consumer confidence. Outbound travel is discretionary. RMB affordability, household confidence, employment expectations, and premium-consumption appetite all influence where travelers go and how much they spend.

Destination sentiment and visa friction. Country-level outcomes can diverge sharply from the total market. Visa access, political sentiment, safety perception, and destination reputation can shift Chinese demand quickly.

What this means for marketers

The main implication is simple: do not plan China outbound around arrivals alone.

A high-volume market may not be the highest-value market. A smaller long-haul corridor may deliver more commercial value per trip. A shopping-heavy market needs a different plan from a beach-leisure market. A repeat-travel corridor needs different messaging from a first-time long-haul destination.

For 2026, commercial teams should focus on five actions.

1. Prioritize markets by spend and fit, not only size

Use arrivals to understand reach, but use spend intensity, audience quality, and category fit to decide where to invest.

2. Treat shopping-linked markets separately

Travel retail, duty-free, luxury, beauty, wellness, and premium retail require their own planning. These categories are influenced heavily before departure through content, social proof, offers, and itinerary design.

3. Win earlier in the journey

Chinese outbound decisions are shaped before departure through search, OTAs, Xiaohongshu, Douyin, WeChat, KOL/KOC content, destination storytelling, and price-value cues. Waiting until arrival misses too much of the funnel.

4. Build corridor-specific playbooks

Hong Kong, Macao, Japan, Korea, Thailand, France, Singapore, Australia, and the US do not compete in the same way. Each corridor needs a different plan across awareness, booking conversion, retail capture, and repeat engagement.

5. Use scenarios for budget planning

Budgets should be stress-tested. If airfares rise, capacity tightens, sentiment shifts, or routes recover faster than expected, the right destination mix changes.

For 2026 planning, the priority is clear: choose markets by spend potential, validate access and route strength, build shopping-linked plans separately, and prepare budget scenarios for airfare and sentiment shifts.

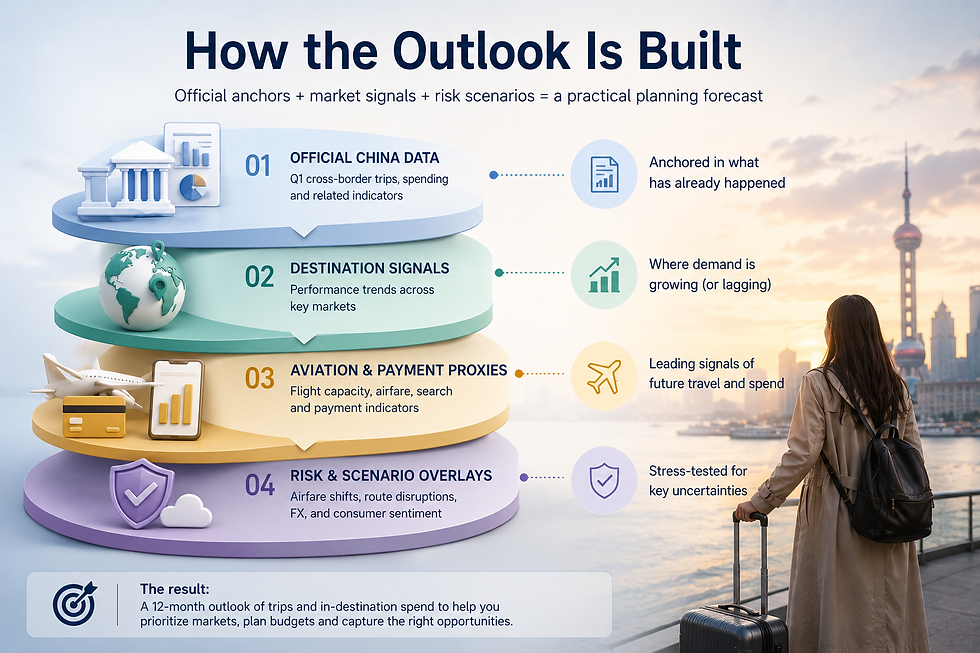

How the outlook is built

The forecast combines official China-side anchors, destination signals, forward indicators, and risk scenarios.

The outlook is a planning forecast, not a live arrivals tracker.

It combines six inputs:

Official China trip data from NIA mainland resident border crossings.

Official China spend data from SAFE Balance of Payments travel debit.

Destination inputs from official or cited country sources where available.

Regional opportunity pools where country-level data is incomplete.

Forward signals from aviation, payment, and market indicators.

Risk scenarios for airfare, route disruption, capacity, FX, consumer confidence, visa friction, and destination sentiment.

The highest confidence sits at the total trip and total spend level. Regional allocation is more directional. Country-level spend should be used for planning, not as audited destination receipts.

That distinction is deliberate. The goal is not to imply precision where open data is limited. The goal is a transparent, usable forecast that helps commercial teams decide where to focus.

The bottom line

China outbound travel in 2026 is moving from recovery to allocation.

The opportunity is not just that more Chinese travelers are going abroad. It is that destinations, retailers, airlines, hotels, and brands now need to compete for where those trips and spend land.

The base planning view points to a large, active market. The high case shows meaningful upside. But the commercial winners will be the teams that focus on the right corridors, influence travelers earlier, and convert intent into spend.

Explore the live 2026 Market Outlook to compare destination opportunity, scenario ranges, shopping-linked value, and current travel risks.

Comments